Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python Information Center

Get comprehensive updates, key reports, and detailed insights compiled from verified editorial sources.

Background on Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python

Tutorial on creating a Black Scholes Merton Model within

Key Details

Explore the primary sources for Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python.

Developments

Stay updated on Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python's latest milestones.

Featured Video Reports & Highlights

Below is a handpicked selection of video coverage, expert reports, and highlights regarding Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python from verified contributors.

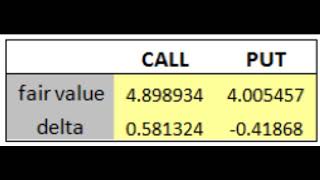

Valuing European Options Using Monte Carlo Simulation Derivative Pricing in Python

Monte Carlo Simulation for Option Pricing with Python (Basic Ideas Explained)

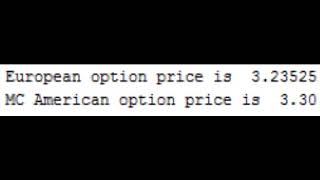

Valuing American Options Using Monte Carlo Simulation –Derivative Pricing in Python

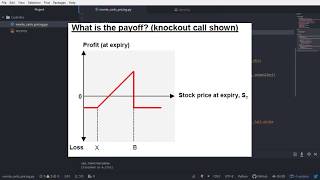

Monte Carlo Pricing Financial Derivatives in Python

Full Guide

Data is compiled from public records and verified media reports.

Last Updated: May 27, 2026

Summary

For 2026, Valuing European Options Using Monte Carlo Simulation Derivative Pricing In Python remains one of the most talked-about profiles. Check back for the newest reports.

Disclaimer:

![MONTE Carlo Simulation in Python for Option Pricing [NEW]🔴](https://i0.wp.com/ytimg.googleusercontent.com/vi/Cb-GwN6jhNE/mqdefault.jpg?resize=320,180)